Mon - Sun 8:00 - 19:00

Mon - Sun 8:00 - 19:00Many patients ask about using super for dental implants and navigating the ATO compassionate release process. The Australian Taxation Office (ATO) legally permits the early release of superannuation to fund critical dental surgeries under strict compassionate grounds. This emergency financial mechanism exists exclusively to treat life-threatening conditions, alleviate acute or chronic pain, or manage severe mental illness when patients have absolutely no alternative means to pay. Cosmetic procedures like routine whitening or elective veneers are categorically excluded. To secure approval, applicants must submit two rigorous medical reports—one from a general practitioner and one from a dental or medical specialist—proving clinical necessity. Processing through myGov typically takes fourteen to twenty-eight days. However, withdrawals are not tax-free. They incur an average withholding tax of twenty-two percent. Patients must navigate these regulations carefully to access necessary restorative care without falling victim to predatory financial practices highlighted by 2026 Ahpra guidelines.

The Hidden Cost of the Dental Crisis in Australia

In 2025 and 2026, the Australian cost of living crisis hit hard. Inflation soared. Essential services rapidly transformed into unaffordable luxuries for a vast segment of the population. The domestic healthcare system, particularly the Medicare framework, offers virtually no safety net for major restorative dentistry. This creates a massive structural gap in public health provision. A single dental implant procedure in metropolitan hubs like Sydney, Melbourne, or Brisbane routinely demands between $3,000 and $7,000 AUD.

For patients requiring comprehensive full-mouth reconstructions, such as the All-on-4 or All-on-6 protocols, the financial burden becomes astronomical. These advanced procedures can easily drain between $20,000 and $60,000 AUD from a patient’s savings. Patients are trapped. They face a devastating, binary choice. Endure excruciating, daily physical pain and systemic health deterioration, or completely liquidate their life savings.

Approximately eighty percent of the Australian population experiences severe financial stress when confronted with unexpected, high-cost dental invoices. Consequently, thousands are forced to systematically delay urgent treatments. This delay inevitably exacerbates the underlying pathology, turning minor cavities into profound pulpal infections, and localized gum disease into catastrophic periodontitis. As the clinical situation worsens, the required interventions become far more invasive and exponentially more expensive. This vicious cycle has driven an unprecedented surge in applications seeking alternative funding mechanisms, placing the nation’s retirement savings system under immense pressure.

What is the Compassionate Release of Superannuation (CRS)?

The Australian superannuation system functions as a strictly regulated, mandatory savings vehicle designed explicitly to ensure financial independence and security during a citizen’s retirement years. Formidable legislative barriers deliberately prevent the early withdrawal of these accrued funds. Exceptions to this rule do not exist outside of explicitly defined statutory parameters. The Compassionate Release of Superannuation (CRS) program represents one of these rare, heavily guarded exceptions.

Administered exclusively by the Australian Taxation Office (ATO), the CRS program provides a critical, last-resort safety net for individuals facing insurmountable medical crises and associated expenses. The volume of applications traversing this system has surged dramatically over recent years. During the 2022-2023 financial year, the ATO received a staggering 75,600 applications for early release across all eligible categories. From this immense pool, assessors approved 41,800 requests, resulting in the total release of $761.7 million AUD from retirement accounts.

A highly significant, rapidly expanding segment of these approved applications specifically funds complex dental treatments. In the preceding year alone, 21,790 individuals successfully unlocked their superannuation to finance critical dental interventions, withdrawing a cumulative total of $526.4 million AUD specifically for oral health. This specific data point speaks volumes. It highlights the profound lack of structural support for advanced dental care within the Australian public health system. Furthermore, it underscores the harsh reality that an increasing number of citizens are being entirely priced out of private health insurance premiums, particularly those comprehensive policies that cover complex implantology and major prosthodontics.

The Four Pillars of ATO Eligibility

The ATO enforces a rigid, uncompromising framework of four fundamental conditions. These conditions must be simultaneously satisfied to approve any compassionate release request. Failure to meet even a single condition results in immediate, non-negotiable application rejection. Assessors operate under strict legislative mandates. They possess absolutely zero discretionary power to waive, modify, or bypass any of these foundational requirements, regardless of the applicant’s personal circumstances.

Table 1: The Four Statutory Conditions for Compassionate Release

| ATO Condition | Statutory Requirement | Clinical and Administrative Implications |

| Condition 1 | Citizenship or Residency Status | The applicant must be, or have historically been, an Australian citizen, a permanent resident of Australia, or a New Zealand citizen. Temporary visa holders are categorically excluded. |

| Condition 2 | Specific Compassionate Grounds | The application must meticulously align with the exact legislative criteria. For dental purposes, this strictly means medical treatment to alleviate severe pain, mental illness, or life-threatening conditions. |

| Condition 3 | Unpaid Expense Status | The medical expense must remain entirely unpaid at the moment of ATO assessment. Reimbursement for previously paid bills is strictly prohibited, preventing individuals from reimbursing personal savings. The only exception occurs if the bill was paid via a formal, outstanding loan specifically secured for that medical purpose. |

| Condition 4 | Total Financial Incapacity | The applicant must definitively demonstrate a genuine, absolute inability to pay the required expense through any other means. This involves proving an absence of sufficient accessible savings, an inability to liquidate non-essential assets, and a lack of access to standard credit facilities. |

For individuals seeking comprehensive restorative dentistry, such as implant-supported bridges, Condition 2 demands the most rigorous clinical substantiation. The proposed treatment must be deemed an absolute medical necessity. Furthermore, the legislation demands proof that the required treatment is not readily available through the public health system within a clinically appropriate timeframe. Given the widely acknowledged systemic limitations, massive waiting lists, and chronic underfunding of the public dental infrastructure in Australia, complex rehabilitative procedures like bilateral implantology frequently and easily meet this unavailability criterion.

To clarify this complex bureaucratic journey, understanding the precise sequence of administrative events is vital. Visualizing the workflow helps applicants prevent critical procedural errors.

Medical Necessity vs. Cosmetic Desires: The Hard Line

Distinguishing between a medical necessity and a cosmetic enhancement requires objective, evidence-based clinical assessment rather than subjective patient preference. The ATO unequivocally prohibits the withdrawal of protected retirement savings for procedures deemed purely cosmetic.

The Australian Dental Association (ADA) robustly echoes this strict prohibition. They note with deep concern that treatments marketed purely for aesthetic alignment, routine tooth whitening, or the placement of elective porcelain veneers fall entirely outside the intended legal definition of compassionate grounds. Unscrupulous practitioners actively advertising on social media that “anyone can access super to fund a new smile” are operating against the spirit of the ATO rules and violating the broader ethical codes of the healthcare profession. A compassionate release super dental claim must be rooted in pathology, not vanity.

Conversely, restorative implantology frequently crosses the definitive threshold into absolute medical necessity. Consider a patient suffering from advanced, aggressive periodontitis. This bacterial infection systematically destroys the periodontal ligaments and the supporting alveolar bone. This leads to widespread, severe tooth mobility and eventual, inevitable extraction. The resulting edentulism (complete or partial tooth loss) causes profound functional impairment.

The physical inability to masticate food properly initiates a devastating cascade of systemic health issues. Without the ability to chew fibrous vegetables and high-quality proteins, patients suffer from severe gastrointestinal distress, chronic indigestion, and long-term systemic nutritional deficiencies. Furthermore, the exposed, unprotected gingival tissues often suffer from chronic, painful ulcerations and recurrent secondary infections caused by the friction of poorly fitting, traditional acrylic dentures. This documented, verifiable pathological cascade validates the medical necessity of placing titanium implants.

The distinction must be clear to both the assessing clinician and the ATO auditor.

The Biology of Tooth Loss and Chronic Pain

Understanding the precise biological and anatomical consequences of tooth loss remains absolutely critical for substantiating a CRS application. A successful application relies heavily on translating complex anatomical degradation into a compelling narrative of chronic pain and functional loss.

When a natural tooth is extracted, the surrounding alveolar bone in the jaw loses the vital, continuous mechanical stimulation previously provided by the periodontal ligament during the act of chewing. Bone is not a static material; it is living, dynamic tissue. Without this constant biomechanical stress, a physiological process known as bone remodeling becomes deeply unbalanced. The osteoclasts—specialized cells responsible for breaking down and absorbing bone tissue—begin to drastically outpace the osteoblasts, the cells responsible for synthesizing and building new bone.

This cellular imbalance initiates rapid, irreversible bone resorption. Within the first twelve months following an extraction, the alveolar ridge can lose up to twenty-five percent of its horizontal width and suffer a highly significant reduction in vertical height.

The Collapse of the Jaw and Nerve Compression

This continuous, aggressive degradation of the jawbone profoundly alters the entire maxillofacial structure. Patients often experience a severe collapse of their vertical dimension of occlusion—essentially, the lower third of their face visibly shrinks. This structural collapse places abnormal, destructive stress on the temporomandibular joint (TMJ). This biomechanical dysfunction results in chronic myofascial pain radiating through the neck and shoulders, debilitating tension headaches, and localized, highly painful joint inflammation.

Furthermore, as the protective bone recedes over time, highly sensitive nerve bundles become dangerously exposed. In the lower jaw (mandible), the inferior alveolar nerve becomes increasingly superficial. When a patient attempts to wear traditional, non-implant-supported dentures, the hard acrylic base presses directly down onto these exposed, unprotected nerves during every single chewing motion. This mechanism causes excruciating, electric-shock-like chronic pain.

Proving “Acute or Chronic Pain” to the ATO

Documenting this specific etiology of nerve compression and joint dysfunction is exactly what transforms a standard dental procedure into a medically necessary intervention under the strict ATO guidelines.

It is strictly required to prove chronic pain for the early release of superannuation. Vague descriptions of discomfort will result in immediate rejection. An application must meticulously detail how the proposed surgical implant strategy will definitively alleviate this documented, specific physiological suffering.

By surgically anchoring a biocompatible titanium or zirconia post directly into the remaining bone, implants artificially restore the necessary mechanical stimulation. This process, known as osseointegration, halts further bone resorption. Crucially, the implants bear the entire occlusal load of chewing, completely alleviating the crushing nerve compression caused by traditional dentures resting on the gums. This mechanical reality forms the undisputed core of a successful compassionate release argument.

The Psychological Toll: Mental Illness and Dental Decay

Beyond the agonizing physical pain, the ATO explicitly recognizes that severe dental degradation can precipitate, exacerbate, or significantly prolong an acute or chronic mental illness.

The psychological devastation of severe edentulism cannot be overstated. Missing multiple anterior (front) teeth or suffering from severe facial collapse due to bone loss often leads to profound social withdrawal. Patients frequently develop debilitating social anxiety, refusing to eat in public, speak in meetings, or engage in normal interpersonal relationships. This chronic isolation frequently triggers severe, medically diagnosable depressive episodes. The intense social stigma associated with visible dental decay compounds this suffering, trapping the patient in a cycle of shame and mental deterioration.

The Psychiatric Reporting Mandate

If an applicant chooses to pursue compassionate release specifically under the “mental illness” clause, the evidentiary burden shifts significantly and becomes substantially more rigorous. The medical documentation must definitively, causally link the two conditions. It must prove that the current dental condition is the primary, driving catalyst for the psychiatric distress, and that the proposed restorative treatment will significantly alleviate the diagnosed mental illness.

In these highly complex, psychologically driven cases, a report from a general practitioner or a general dentist is entirely insufficient. The ATO legally mandates that the specialist report must be completed specifically by a registered psychiatrist. This psychiatrist must conduct a comprehensive evaluation, officially diagnose the mental illness, and sign the legal declaration stating that the dental surgery is a necessary psychiatric intervention. A report from a registered psychologist, while clinically valuable, does not satisfy this strict ATO legislative requirement; it must be a medical doctor specializing in psychiatry.

Navigating the Medical Reporting Requirements

The structural integrity and ultimate success of a CRS application rest entirely upon the quality, precision, and completeness of the medical evidence provided. The ATO operates as a tax collection agency, not a medical board. Therefore, they rely absolutely on the written testimony of registered healthcare professionals. They will aggressively reject any application lacking the precise, statutory documentation. For dental interventions, the law dictates the mandatory submission of two independent, corroborating medical reports.

The Dual Report Requirement

The legislation requires one report from a registered general practitioner (GP) or a general dental practitioner. The second, corroborating report must originate from a registered medical or dental specialist.

Crucially, this specialist must hold formal, recognized registration with Ahpra in the specific clinical field relevant to the proposed treatment. In the complex context of reconstructive implantology, this typically necessitates a highly detailed report from a recognized Prosthodontist, an Oral and Maxillofacial Surgeon, or a Periodontist.

Both practitioners must independently evaluate the patient and formally certify that the proposed treatment is absolutely necessary to treat a life-threatening illness, alleviate acute or chronic pain, or alleviate an acute or chronic mental illness. Furthermore, both professionals must explicitly attest that the required treatment is not readily accessible through the public healthcare system.

Table 2: Required Documentation Portfolio for ATO Assessment

| Document Type | Specific Statutory Requirements | Validity Period |

| General Medical Report | Completed by a GP or General Dentist using the official Form NAT 74927. Must outline the chronic pain or mental illness. | Must be signed and dated less than 6 months prior to the exact date of application submission. |

| Specialist Medical Report | Completed by a relevant Specialist (e.g., Prosthodontist, Oral Surgeon, or Psychiatrist). Must corroborate the GP’s findings. | Must be signed and dated less than 6 months prior to the exact date of application submission. |

| Comprehensive Treatment Plan | A highly detailed clinical roadmap outlining all surgical stages (e.g., bone grafting, fixture placement, abutment connection). | Must perfectly align with the dates and procedures mentioned in the medical reports. |

| Itemized Clinical Invoice | An exact, granular breakdown of all surgical and prosthetic costs. A vague, lump-sum estimate will trigger an instant rejection. | Must remain entirely unpaid at the precise time the ATO conducts its assessment. |

Documentation Validity and Form NAT 74927

To standardize this rigorous evidentiary process and reduce administrative errors, the ATO provides a specific, mandated document: the Compassionate release of superannuation – Report by registered medical practitioner (Form NAT 74927).

Utilizing this exact, formatted form is not merely a suggestion; it is the most effective way to mitigate the risk of inadvertently omitting mandatory statutory declarations. The form requires the practitioner’s Ahpra registration number, practice details, and a formal declaration of truth.

Timing is critical. Both medical reports must be completed, signed, and dated no more than six months before the official submission date of the application via the myGov digital portal. If a patient gathers their reports in January but waits until August to apply, the evidence is legally void. They must return to the specialists, undergo new clinical consultations, and pay for entirely new documentation. If the medical reports are incomplete, lack sufficient clinical detail, or omit the specialist’s Ahpra number, the processing of the application will be severely delayed, or it will face outright rejection.

Recognizing Predatory Practices in 2026

The unprecedented surge in superannuation withdrawals for dental care has triggered massive alarm across all major regulatory bodies. The Australian Health Practitioner Regulation Agency (Ahpra), the Dental Board of Australia, and the ATO have issued stern, joint warnings regarding the ethical obligations of practitioners participating in the CRS process.

The core of this regulatory concern centers on the urgent protection of financially and medically vulnerable patients. These individuals, desperate for pain relief, may be easily coerced into prematurely depleting their crucial retirement reserves for treatments that are vastly overpriced, clinically unnecessary, or overly aggressive.

Identifying the Red Flags of Exploitation

Ahpra has explicitly identified several critical “red flags” indicative of predatory behavior within the dental sector. Regulatory scrutiny intensifies exponentially when corporate dental clinics actively promote superannuation withdrawal as their primary marketing tool and sales closer, rather than treating it as the last-resort financial safety net it was legally designed to be.

Table 3: Regulatory Red Flags for Predatory Dental Practices

| Predatory Practice | Clinical Impact and Regulatory Concern |

| Telehealth-Only CRS Assessments | Conducting evaluations for complex, invasive surgical implants entirely via video call, without vital physical palpation or 3D radiographic examination, severely undermines clinical accuracy and safety. |

| Aggressive Upfront Payment Demands | Pressuring vulnerable patients to pay massive, non-refundable deposits before the ATO has even approved the application violates core financial consent principles. |

| Upselling Unnecessary Procedures | Aggressively recommending $50,000 full-mouth premium reconstructions when localized, cheaper, conservative interventions (like a single bridge) would suffice to eliminate the pain. |

| Requesting myGov Login Credentials | A severe, illegal privacy breach where clinic staff attempt to log into myGov to process the application directly on behalf of the patient to secure their fee. |

The ADA reinforces these strict ethical boundaries. They state unequivocally that dentists are strictly prohibited from providing any form of financial guidance regarding the long-term economic implications of withdrawing superannuation. Dentists are clinicians, not accountants. Such complex financial advice must only originate from qualified professionals holding a valid Australian Financial Services License.

Furthermore, the ADA clarifies a crucial logistical point: the clinician who authors the ATO support report is not legally bound to be the same clinician who eventually executes the surgical treatment. This deliberate separation of clinical assessment from surgical execution helps eliminate dangerous financial conflicts of interest, ensuring the recommendation is based purely on patient need, not clinical profit.

Informed Financial Consent and Exploring Alternatives

Before initiating any aspect of a treatment plan tied to a CRS application, practitioners must secure absolutely airtight, informed financial consent. This ethical mandate requires complete, brutal transparency. The dentist must clearly outline the total cost of the initial surgery, the cost of the final ceramic prosthetic restorations, and, crucially, the anticipated, lifelong maintenance costs of the implants (such as professional cleaning, potential screw replacements, and radiographic monitoring).

Patients must be actively presented with a full spectrum of treatment alternatives. This includes thoroughly discussing less expensive, conservative options, even if those options are less than ideal aesthetically. This ensures that the monumental decision to pursue implantology and liquidate hard-earned retirement funds is made with absolute cognitive clarity and uncoerced autonomy.

The Financial Reality: Taxation and Hidden Impacts

The decision to access superannuation a decade or more before retirement carries profound, irreversible financial consequences. In their desperation to escape dental pain, patients frequently misunderstand the taxation mechanics applied to these early withdrawals.

Crucially, funds released on compassionate grounds do not arrive in the patient’s bank account tax-free. They are subject to significant taxation, which must be factored into the initial application amount.

Understanding Withholding Tax and Marginal Rates

When the ATO assesses and approves a compassionate release application, the applicant’s specific superannuation fund acts as the designated withholding agent. The fund is legally required to deduct tax before transferring the money to the patient.

The exact tax rate is not a flat fee; it fluctuates based on the applicant’s age, their specific fund structure, and the underlying components of their superannuation balance (specifically, the ratio of taxable to tax-free components). However, historical data and financial counseling guidelines indicate that, on average, a withholding tax of approximately twenty-two percent is automatically deducted. Depending on highly specific individual tax circumstances, this withholding tax can legally reach up to a punishing thirty-two percent.

Applicants must meticulously account for this significant tax burden when requesting funds. Consider this scenario: A patient receives a surgical invoice totaling exactly $20,000 AUD. If they log into myGov and request exactly $20,000 from their fund, the fund will deduct 22% ($4,400) for tax. The patient will only receive $15,600 in their bank account, leaving them $4,400 short of paying their surgeon.

Therefore, the application must strategically request a gross amount sufficient to cover both the clinical invoice and the anticipated withholding tax. Only by calculating this grossed-up figure can the patient ensure the final, net disbursement adequately covers the outstanding medical debt.

Verification of Fund Policies and Account Balances

The ATO explicitly instructs all applicants to proactively contact their specific superannuation fund long before initiating a myGov application. This is a critical, often-missed step. Not all superannuation trust deeds permit early release on compassionate grounds. While the law allows it, individual funds govern their own trust rules. The fund administrators possess the ultimate, unchallengeable authority to deny a withdrawal, even if the ATO has issued a formal approval letter.

Applicants must verify four critical elements with their fund provider during a phone call :

-

Policy Allowance: Explicit confirmation that the fund’s governing rules actually allow early release for compassionate medical reasons.

-

Balance Verification: Verification that there is a sufficient account balance to cover the massive gross requested amount (the invoice plus the heavy taxes).

-

Administrative Fees: Clarification of any hidden administrative fees levied by the fund for manually processing the early withdrawal.

-

Insurance Implications: A deep understanding of how withdrawing a substantial lump sum might catastrophically impact attached insurance policies. Many Australians hold their life insurance and income protection insurance within their super. These policies are often tied to maintaining minimum account balances; dropping below that balance can instantly cancel the insurance policy.

Furthermore, accessing super early permanently removes that capital from the market. This destroys years of potential compound interest. A $20,000 withdrawal at age forty could equate to a $60,000 or $80,000 reduction in the final retirement balance at age sixty-five. Additionally, withdrawing a large lump sum can severely alter an individual’s income and asset tests, potentially reducing or immediately canceling ongoing Centrelink support payments or altering child support calculations.

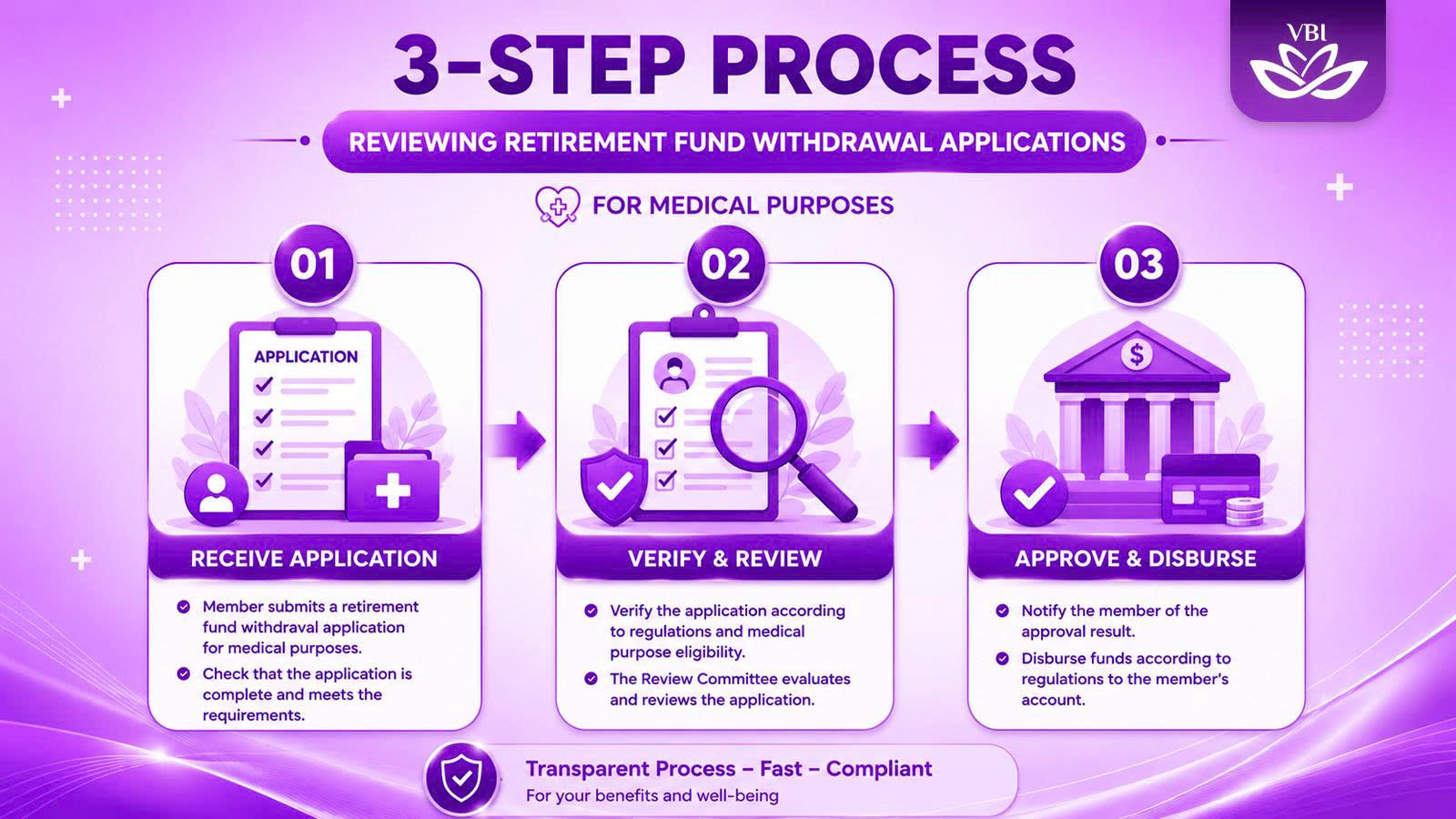

Step-by-Step: Submitting Your Application on myGov

Executing a flawless application requires strict adherence to administrative procedures. The entire process is conducted digitally through the Australian Government’s centralized myGov portal, which links directly to the ATO’s internal assessment services. Paper applications exist but cause severe processing delays.

Pre-Application Preparation and Evidence Gathering

Before even logging into the digital portal, the applicant must physically compile the entirety of their evidentiary portfolio. This includes the two completed, signed, and dated NAT 74927 medical reports. It includes the highly detailed clinical treatment plan. Most importantly, it requires the itemized, entirely unpaid invoice from the dental provider.

This invoice must be a masterpiece of clarity. It must clearly demarcate each chronological stage of the complex implant procedure. It must separate surgical costs (such as sinus lifts, bone grafting materials, and titanium fixture placement) from the subsequent prosthetic costs (custom abutments and zirconia crowns).

If the applicant is seeking to release their funds to pay for the treatment of a dependent (such as a spouse suffering from severe periodontitis or a child needing massive maxillofacial reconstruction after trauma), they face an additional hurdle. They must gather and upload definitive documentary evidence proving the dependent relationship, such as marriage certificates, shared utility bills, or birth certificates.

Submission, Assessment Timelines, and Decision Reviews

Once the documentation is successfully uploaded in PDF format and the digital legal declaration is signed, the ATO commences its rigorous assessment. The standard processing timeframe spans between fourteen and twenty-eight days. During this tense waiting period, ATO medical assessors frequently contact the authoring medical practitioners directly via phone to verify the authenticity of the reports and the severity of the clinical claims.

If the application survives this scrutiny and is approved, the ATO dispatches a formal, digitally signed approval letter directly to the applicant’s myGov inbox. The ATO’s involvement ends here. The ATO does not transfer the money. The applicant must then download this specific authorization document and forward it directly to their superannuation fund to trigger the actual financial disbursement. Super funds have their own internal processing times, adding further days to the wait.

In instances where an application is aggressively rejected—usually due to insufficient clinical evidence, vaguely written invoices, or failure to meet the strict statutory criteria—the applicant retains the legal right to request a formal review of the decision. This review request must generally be lodged within a strict fourteen-day window following the date of the original rejection letter. The review must be accompanied by a highly detailed, written explanation outlining exactly why the initial ATO assessment was factually incorrect based on the provided clinical evidence.

Taking Your Super Overseas: The Vietnam Advantage

The astronomical, often prohibitive cost of complex implantology within the domestic Australian market has catalyzed a massive, structural shift toward international medical tourism. Faced with $40,000 invoices at home, thousands of Australians are actively seeking world-class treatment in Southeast Asian medical hubs. This prompts a vital, frequently asked legal question: Can you use Australian superannuation to fund offshore healthcare?

The Regulatory Stance on Offshore Medical Interventions

The Australian legislation governing the ATO does not explicitly prohibit the use of compassionate release funds for overseas medical treatment. However, the evidentiary burden remains identical to a domestic claim, and in administrative aspects, it becomes significantly more complex.

The two mandatory medical reports must still be completed, signed, and authorized by registered Australian practitioners. These local, Ahpra-registered doctors must evaluate the patient’s severe condition, certify the absolute necessity of the treatment to alleviate chronic pain, and confirm that the required treatment is not readily available in the public system.

The administrative complexities arise when presenting the itemized invoice. The chosen overseas clinic must provide highly detailed, professionally translated documentation (in English) that clearly outlines the exact surgical protocol. Crucially, this offshore treatment plan must perfectly match the clinical recommendations endorsed by the Australian practitioners in their reports.

To explore the profound macroeconomic disparities driving this massive exodus of dental patients, individuals routinely conduct exhaustive research into international pricing structures. Resources analyzing the dental implant cost in vietnam demonstrate a staggering reality. Comprehensive, full-mouth restorations using premium Swiss or American materials can be flawlessly executed for a mere fraction of the domestic Australian price. This remains true even when factoring in the auxiliary costs of premium return flights, luxury hotel accommodation, and local transport in Hanoi.

This cost differential represents a massive strategic advantage. By accessing treatment in Vietnam, the patient needs to withdraw a vastly smaller lump sum from their superannuation. This inherently protects a much larger portion of their long-term retirement balance from early liquidation and the associated massive tax penalties.

Maintaining Clinical Continuity and Post-Operative Care

When patients leverage the early release of superannuation for offshore surgical procedures, meticulous, paranoid planning regarding postoperative care becomes absolutely paramount. Dental implants are not magical; they require a prolonged, vulnerable biological integration phase (osseointegration) lasting three to six months. They also require meticulous, daily hygiene maintenance to prevent a devastating bacterial infection known as peri-implantitis.

Top-tier international facilities, particularly specialized, elite implant centers located in Vietnam, counter these risks by adhering strictly to global standards. They operate under rigorous international infection control protocols, exactly mirroring those set by the Association for the Advancement of Medical Instrumentation (AAMI).

Furthermore, these elite clinics provide patients with comprehensive “International Implant Passports.” This vital document details the exact specifications, lot numbers, and dimensions of the specific titanium fixtures utilized during surgery (e.g., premium brands like Straumann or Nobel Biocare). This documentation is not a souvenir; it is a clinical necessity. Should a minor mechanical complication arise—such as a loosened abutment screw—once the patient returns home to Australia, local practitioners desperately require this specific, technical data to source compatible prosthetic components and provide safe, necessary interventions.

For a comprehensive, legally binding overview of the official expense eligibility rules, all prospective patients must consult the primary government legislative resources detailing the early release of superannuation.

Frequently Asked Questions (FAQ)

Can I withdraw superannuation for cosmetic dental procedures like veneers?

No, absolutely not. The ATO strictly and categorically prohibits accessing protected retirement funds for any treatments deemed purely cosmetic. This includes elective porcelain veneers, routine teeth whitening, and minor orthodontic alignments. To qualify under the strict legislative framework, the proposed treatment must definitively alleviate acute or chronic physical pain, manage a severe mental illness, or treat a life-threatening pathology. Vanity is never considered a compassionate ground under Australian tax law.

Do I really need a specialist report to apply for dental implants, or is my local dentist enough?

Yes, a specialist report is a non-negotiable legal requirement. The legislation explicitly mandates the submission of two distinct medical reports to prevent fraud and ensure clinical validity. While the first report can originate from a general dentist or a general medical practitioner (GP), the second corroborating report must be authored by a registered specialist operating in the relevant clinical field (such as an Ahpra-registered Prosthodontist, Periodontist, or Oral and Maxillofacial Surgeon). Both must independently verify the medical necessity of the implants.

Exactly how much tax will be deducted from my approved superannuation withdrawal?

The final tax rate fluctuates based on highly individual factors, including your exact age and the specific ratio of taxable to tax-free components within your super account. However, on average, a severe withholding tax of approximately twenty-two percent is automatically deducted by the superannuation fund prior to any money hitting your bank account. In certain high-income brackets, this penalty can reach thirty-two percent. You must calculate this tax loss when deciding how much gross money to request on your myGov application.

Can I get reimbursement for massive dental bills I have already paid out of my savings?

Generally, no. Condition 3 of the stringent ATO guidelines explicitly dictates that the medical expense must remain entirely unpaid at the exact moment of application. The CRS program is a “last resort” safety net, not a reimbursement scheme. The only legal exception to this rule exists if the medical invoice was previously paid using funds from an outstanding, formally documented loan specifically acquired for that exact medical purpose, and that loan remains unpaid.

How long does the ATO take to process a compassionate release application once submitted?

Standard processing times range from fourteen to twenty-eight business days, provided the application is submitted digitally via the myGov portal with all correct PDF attachments. Paper applications sent via postal mail face significantly longer processing times. Additional, severe delays frequently occur if the ATO assessors need to verify complex clinical data directly with the authoring medical practitioners via phone calls, or if the submitted invoices lack sufficient itemized detail.

Is it legal to use released superannuation funds to pay for dental treatment in Vietnam?

Yes, the ATO legislation does not strictly forbid utilizing approved, released funds for offshore medical treatments, provided the treatment meets all criteria. However, the initial medical reports justifying the deep clinical necessity must still be completed and signed by registered Australian medical professionals prior to the application. Furthermore, the overseas clinic must provide highly detailed, English-translated treatment plans and invoices that perfectly match the Australian doctors’ recommendations.

What happens if my superannuation fund refuses to release the money, even with ATO approval?

This is a highly distressing, but entirely possible scenario. Even armed with an official ATO approval letter, the final financial disbursement decision rests entirely with the superannuation fund’s specific governing trust rules. If a particular fund’s internal policies strictly prohibit early release for any reason, the applicant cannot force them to pay. In this frustrating situation, the patient may need to explore rolling their entire super balance over to a different, more accommodating retail or industry superannuation fund before reapplying.

Will withdrawing my super early affect my government Centrelink payments?

Yes, it is highly probable and represents a significant secondary financial risk. Withdrawing a massive lump sum (e.g., $30,000 for full-mouth implants) can violently alter an individual’s government income and asset tests. This sudden influx of cash can potentially reduce, or entirely cancel, ongoing Centrelink support pensions, family tax benefits, or significantly alter child support liability calculations. Professional, independent financial counseling is strongly advised prior to submitting any application.

Are cheap telehealth consultations sufficient for getting the specialist medical report?

Ahpra has issued severe, public warnings against relying solely on quick telehealth appointments for complex surgical assessments. While telehealth serves a purpose for basic triage, evaluating jawbone density, nerve proximity, and structural requirements for complex dental implants fundamentally requires a physical, in-person examination and advanced 3D radiographic (CBCT) analysis. Telehealth-only approvals for massive withdrawals are a major red flag for regulatory audits.

How long are the medical reports legally valid for the myGov application?

Timing is absolutely critical. Both the general practitioner’s report and the specialist’s report (Form NAT 74927) must be signed and dated no more than exactly six months prior to the date the application is officially submitted to the ATO via the portal. If the reports expire by even one day, the system will reject the application, forcing the patient to acquire entirely new, costly medical documentation.

Can a dental clinic log in and apply for the early release on my behalf to save time?

No. Clinics actively requesting a patient’s personal myGov login credentials to process applications rapidly are committing a severe privacy breach and engaging in highly illegal, predatory behavior explicitly flagged by Ahpra. The application involves sensitive tax and retirement data. It must be submitted personally by the patient, or by a legally appointed, registered tax agent or financial counselor acting formally on their behalf.

What are my legal options if my application is completely rejected by the ATO?

Applicants possess the strict legal right to request a formal, internal review of the negative decision. This review request must clearly, logically articulate exactly why the initial assessment was factually flawed based on the provided clinical evidence. Crucially, this appeal must generally be submitted within a highly restricted fourteen-day window following the receipt of the original rejection notice in the myGov inbox.

Does the specialist dentist who writes the ATO report have to be the one performing the surgery?

No. The ADA ethical guidelines specify clearly that the clinician assessing the medical necessity and authoring the ATO support report is not legally or ethically obligated to be the same practitioner who eventually executes the surgical treatment plan. This separation is actually encouraged, as it removes the financial conflict of interest, ensuring the recommendation for surgery is based on pathology, not the desire to secure a massive surgical fee.

Can I access my super to pay for my spouse’s or dependent child’s dental treatment?

Yes. The compassionate release legislative framework legally extends to defined dependents (such as spouses, de facto partners, or children). However, the applicant faces an additional administrative burden. They must provide definitive, legal documentary evidence establishing the dependent relationship (e.g., marriage certificates, shared financial statements) alongside the two mandatory medical reports pertaining to the dependent’s condition.

What exact evidence proves “total financial incapacity” to the ATO assessors?

Condition 4 requires applicants to prove they simply cannot afford the expense. The ATO assesses the applicant’s overall, holistic financial position. This requires formal, legally binding declarations that sufficient funds cannot be accessed through personal savings accounts, the liquidation of non-essential assets (like shares or secondary vehicles), or through existing, standard credit facilities (like personal loans or credit cards).

Bài viết liên quan

Dental Implant Failure Symptoms: Causes & How to Fix It

Dental implants represent a highly predictable restorative solution in modern dentistry, but they are not...

The Hidden Risks of Cheap Dental Implants Overseas

Seeking affordable dental care abroad sounds highly appealing. But what are the actual cheap dental...